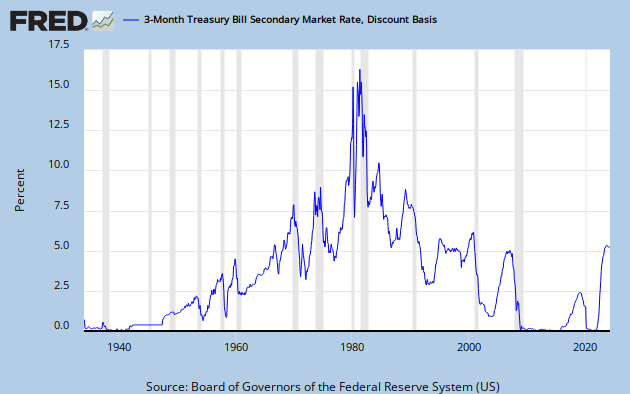

The risk-free rate of return, which is the return on investment that is required as compensation for not having access to the capital for a period of time, is a fascinating theoretical notion from the finance world. In essence, the risk-free rate is trying to untie the time value of money from the risk premium, i.e. the rate of return required in excess of the risk-free rate to account for default risk. Together, these two factors determine the interest rates for all debt obligations. I say that the risk-free rate is a theoretical notion because there is no such thing as a truly risk-free investment. Even 3-month U.S. Treasury bills, the most commonly used proxy for the risk-free rate, still have some remote risk of default (in the event of a nuclear war, the Treasury might miss a payment or two). For context, the graph below shows some historical data on the 3-month U.S. Treasury bill:

The purpose of this post is to question whether it makes sense for finance professionals to use the 3-month U.S. Treasury bill as a proxy for the risk-free rate of return. First, I want to change the time period of the sovereign bonds I will consider from three months to ten years. I am doing this because it is much easier to do a cross-country analysis of 10-year bonds, which almost every debt-issuing country has, than of 3-month bonds. I don’t think this will detract from the validity of my analysis significantly because though there is a higher risk premium associated with a longer time period, it makes sense that the “risk-free” country over the next three months is also the least likely to default over the next ten years.

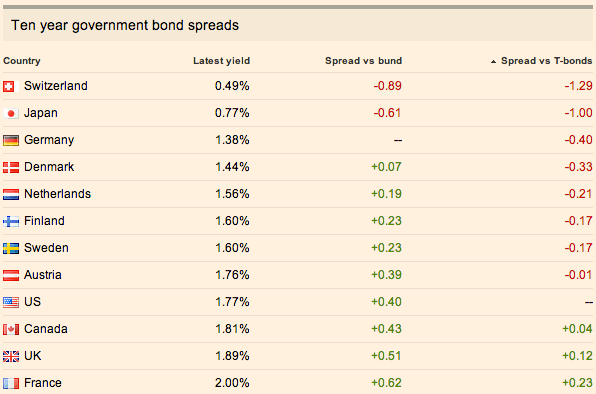

Now let’s look at some data for 10-year government bonds from various countries:

The data above are provided by The Financial Times and you can see updated figures by clicking on the table. The main takeaway from this is that the United States does not have the lowest yield on its 10-year bonds. In fact, as of this writing, there are eight countries who have a lower cost of funds than we do. That means global investors believe the risk associated with those government bonds is lower than the risk associated with U.S. government bonds. They believe those countries are more likely to make all their payments on time than the richest country on earth is. Why is that?

For starters, we have a seriously dysfunctional political system in which artificial crises are manufactured by the two-parties (think debt ceilings and fiscal cliffs) in order to score political points. Many people claim these crises are the only way policymakers in Washington can get anything done anymore. But instead of getting things done, they just end up kicking the can down the road to another unnecessary flashpoint. One of these days, we could end up with a staring contest in which neither party blinks and the Treasury Department is forced to default on some of our debt.

Secondly, the U.S. debt-to-GDP ratio, which represents our ability to pay back our debt, has been rising at an alarming pace over the last decade (we haven’t had a budget surplus since the Clinton Administration). As of yet, there has been no run on the U.S. Treasury (as reflected in our historically low interest rates), and it does not appear as though an attack from the bond vigilantes is imminent. Nevertheless, it can’t help our Treasury yields that our debt-to-GDP ratio is approaching an all time high:

Critics of my argument might point out that Switzerland recently pegged its currency to the euro prevent it from appreciating further and that Japan has a gargantuan debt, coupled with low growth prospects. These reasons might explain why Switzerland and Japan have lower yields on their 10-year bonds, without having to claim they are more “risk-free” than U.S. debt. But what about the other six countries ahead of us on the list? Many of them have strong fundamentals (e.g. low debt, strong growth, current account surplus) and unlike the United States, they are unlikely to default via a gridlocked political system.

So, does it make sense to continue to use the U.S. 3-month Treasury bill yield as a substitute for the theoretical risk-free rate? There are eight countries who have lower yields on their 10-year bonds and many of them appear more stable than the United States. I think it’s about time we reconsidered which country is the least likely to default on a 3-month debt obligation and therefore is the closest to the theoretical risk-free rate of return. Right now, I wouldn’t bet on that being us.